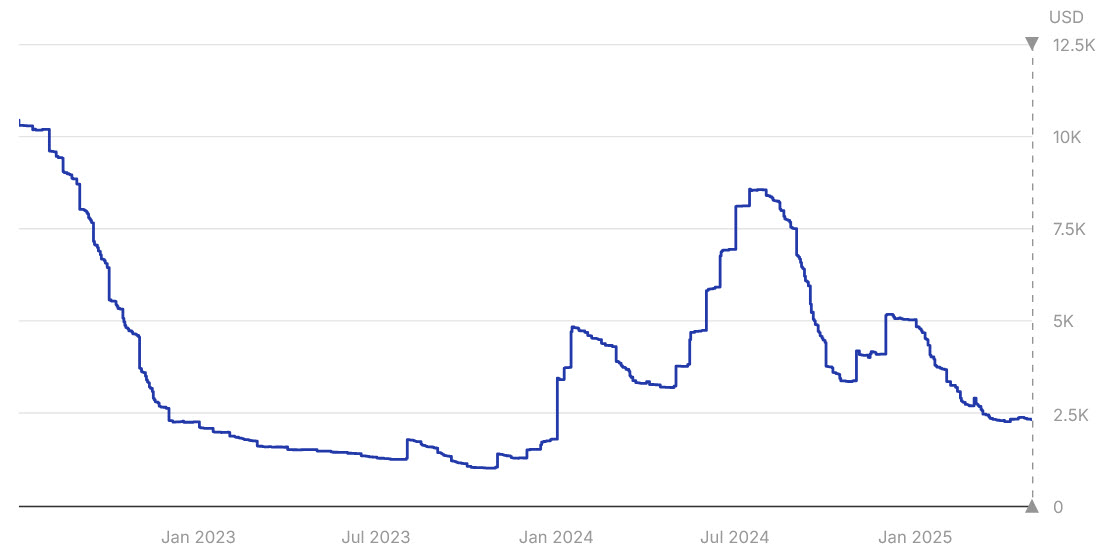

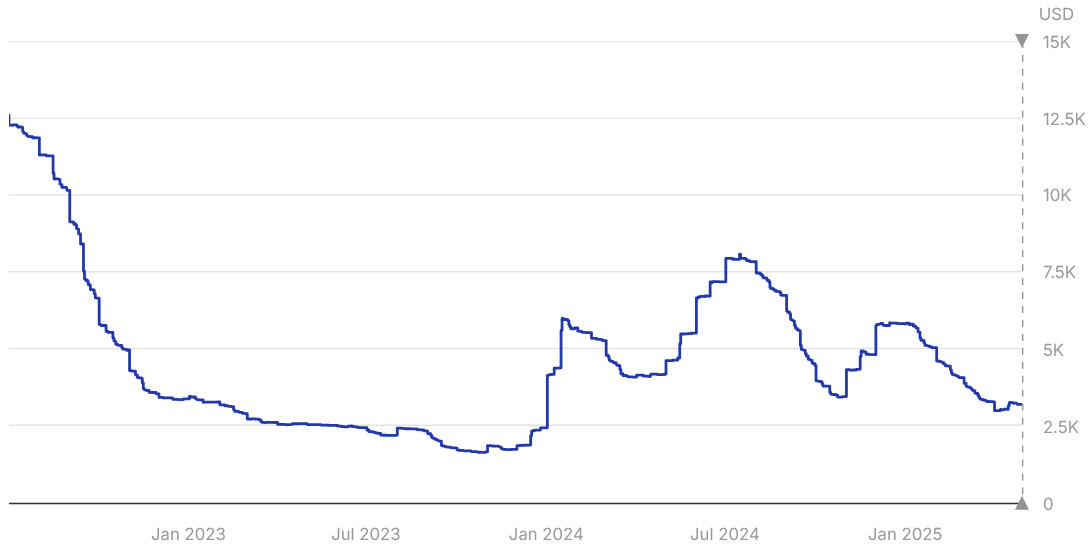

Source: Market average rates for 40‘ containers according to www.xeneta.com

Trade Analysis: Far East Westbound

Situation

Bookings on this trade lane increased toward the end of November and the beginning of December. Although vessel space is getting tighter, rates are holding steady and have not increased significantly in the first half of December. This aligns with the slightly lower SCFI recorded in the final week of November. The current rate stability is primarily due to increased vessel capacity into North Europe – offsetting the impact of announced blank sailings and resulting in more space being available.

Obstacles

For now, the situation remains quite stable, but space is expected to become more limited towards the end of the year as cargo volumes rise ahead of the Lunar New Year (LNY).

Outlook

As usual, we expect a rush before LNY, which will have an even stronger impact on the Mediterranean area due to the Ramadan festivities taking place in the same week. Higher cargo volumes are expected prior to these events. This will further reduce available vessel space in the Mediterranean Sea.

It is also worth noting that shipping companies are closely monitoring the situation in the Red Sea.

A shortcut through the Arctic?

- Insights

Find out more about one of the world’s most remote and probably coldest nautical routes, a “new try” this summer, and why it is still far from being used regularly.

27,500 TEU giants will roam the sea

- Facts

Today’s "maritime monsters" can transport over 24,000 containers and now there are plans for a new record-breaking ship.

A talk with Rolf Habben Jansen, CEO of Hapag Lloyd

We had the opportunity to talk to CEO of the fifth largest container carrier worldwide about the recent developments in seafreight and acquisition plans.