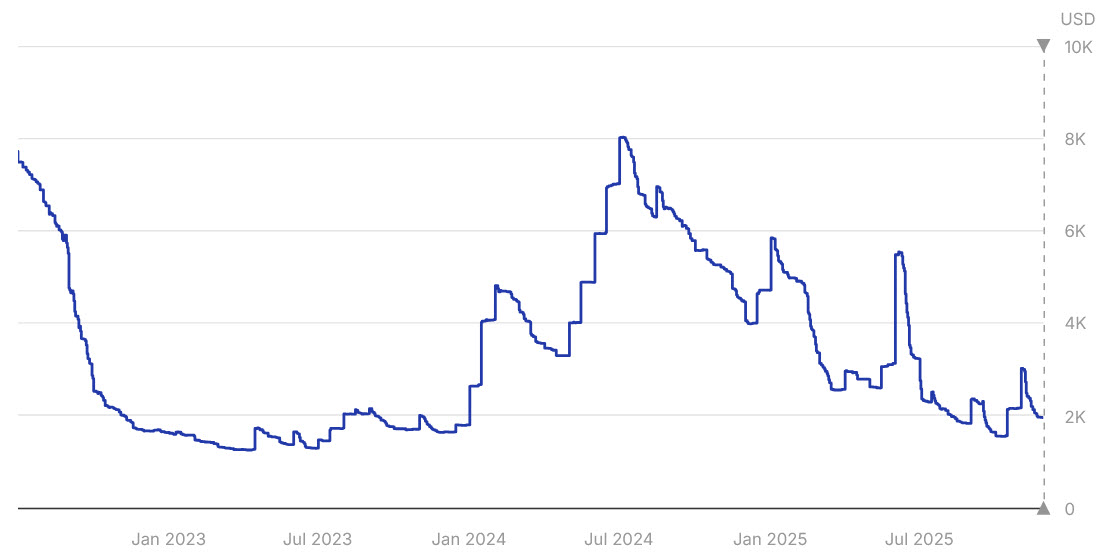

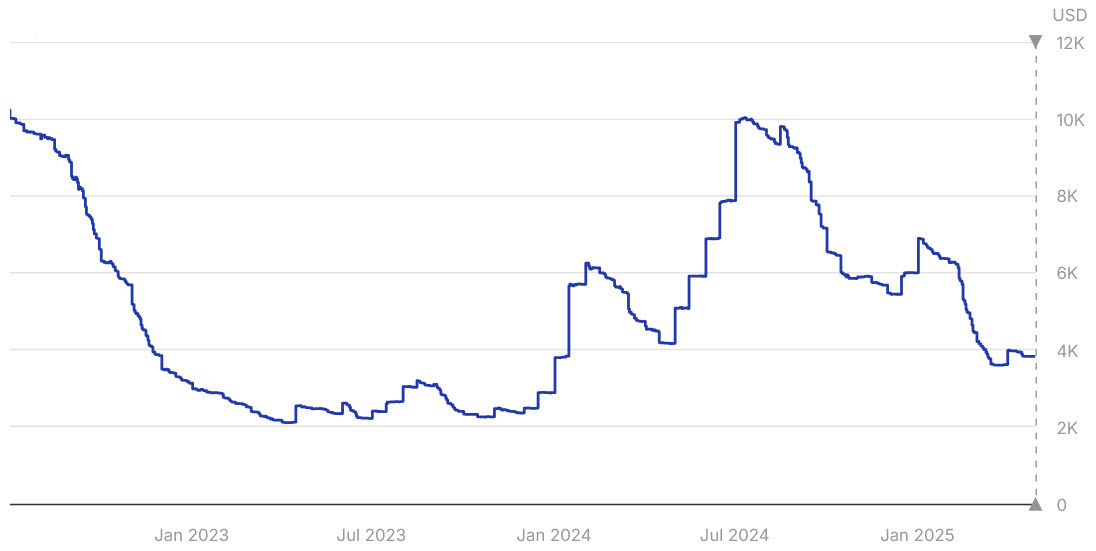

Source: Market average rates for 40‘ containers according to www.xeneta.com

Trade Analysis: Transpacific

Situation

Following a brief peak in November, when rates increased for a short period, we are currently experiencing balanced demand and supply, with more space available, particularly for the US East Coast. Capacity has increased by almost 11%. There has been a continuous weekly rate drop on Transpacific trades, and no peak season is expected in December.

Obstacles

There are currently no major obstacles and no significant challenges at US ports.

Outlook

We expect a short-term increase in cargo volumes prior to the Lunar New Year (LNY), along with further space restrictions during the usual Transpacific tender season in Q1, which could lead to further short-term rate increases. The general outlook for this trade in 2026 is rather flat due to geopolitical reasons. Some companies are focusing more on a “China+1” sourcing strategy, which could increase volumes from Vietnam, Thailand and India along this trade lane.

Panama Canal: When Waterways Lack Water

- Insights

The Panama Canal, which connects two oceans, simply does not have enough water. Delve deeper into maritime traffic jams and how the Suez Canal temporary substituted the Panama Canal.

The amphora: precursor to the ISO container

- Facts

Highly distinctive in shape, their characteristics mean they are regarded as the precursors to today’s shipping containers. Learn more about stacking techniques and the role they played...

27,500 TEU giants will roam the sea

- Facts

Today’s "maritime monsters" can transport over 24,000 containers and now there are plans for a new record-breaking ship.